What You Need To Learn About Mortgages For Your House

Content by-Omar MosesTo a person untrained in the art of real estate, the mortgage financing process can seem incredibly complicated. Although mortgages are difficult to fully understand, by educating yourself on the best mortgage practices you can learn everything you need to know to get a good deal on your mortgage. This article is filled with great mortgage information, so read on to learn more.

Predatory lenders are still in the marketplace. These lenders usually prey on home buyers with less than perfect credit. They offer low or no down payments; however, the interest rates are extremely high. Additionally, these lenders often refuse to work with the homeowner should problems arise in the future.

Before applying for a mortgage, pay down your debts. Lenders use a debt to income ratio to verify that you are able to afford a mortgage. A general rule of thumb is 36 percent of your gross income should be available to pay all of your monthly expenses, including your mortgage payment.

To make your application for a mortgage fast and easy, make electronic copies of your last two pay checks, two recent bank statements, W2s, and tax information. Lenders will ask for all of this information to go with the application and having them on hand in electronic format makes it easy to supply this information.

Know the amount you are paying for closing costs, and remember to itemize. Whether you pay closing costs up front or the costs are added to your loan, you need to know how much you are paying. Sometimes you can negotiate with the seller to split some of the closing costs.

Don't make any sudden moves with your credit during your mortgage process. If your mortgage is approved, your credit needs to stay put until closing. After a lender pulls up your credit and says you're approved, that doesn't mean it's a done deal. Many lenders will pull your credit again just before the loan closes. Avoid doing anything that could impact your credit. Don't close accounts or apply for new credit lines. Be sure to pay your bills on time and don't finance new cars.

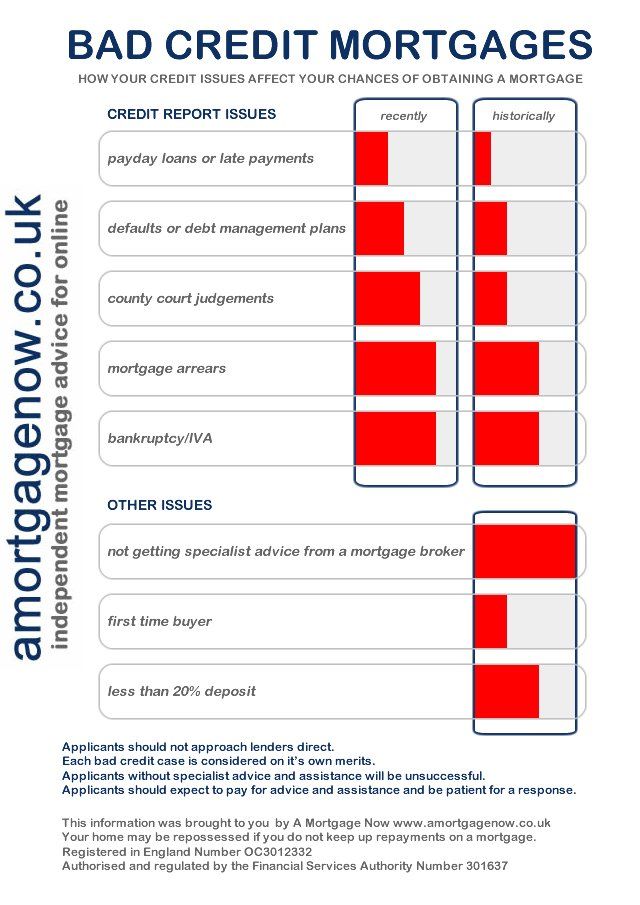

Consider a mortgage broker instead of a bank, especially if you have less than perfect credit. Unlike banks, mortgage brokers have a variety of sources in which to get your loan approved. Additionally, many times mortgage brokers can get you a better interest rate than you can receive from a traditional bank.

Lenders look at your debt-to-income ratio in order to determine if you qualify for a loan. If your total debt is over a certain percentage of your income, you may have trouble qualifying for a loan. Therefore, reduce your debt by paying off your credit cards as much as you can.

Keep on top of your mortgage application by checking in with your loan manager at least once per week. It only takes one missing piece of paperwork to delay your approval and closing. There may also be last minute requests for more information that need to be provided. Don't assume everything is fine if you don't hear from your lender.

If you have bad credit, avoid applying for a home mortgage. Although you may feel financially ready enough to handle the costs of a mortgage, you will not qualify for a good interest rate. This means you will end up paying a lot more over the life of your loan.

Keep your job. Lenders look into many aspects of your financial situation and one very important aspect is your employment income. Stability is very important to lenders. Avoid moving jobs or relocating for as long as possible before you apply for a home mortgage. This will show them that you are stable.

Be sure you have a good amount of money in your saving's account before you try applying for your home's mortgage. You will need to have cash on hand for closing costs, a down payment and such miscellaneous expenses as inspections, application and credit report fees, title searches and appraisals. Having a larger down payment may lead to a mortgage with better terms.

Compare multiple factors as you shop for a mortgage. Clearly, you are interested in finding a low interest rate. In addition, you need to evaluate all types of mortgage products. Closing costs, down payment requirements, and other costs involved in home buying need to be considered, too.

Look into foreclosed homes before you seek out properties that are brand new. Banks don't mind dealing with other banks, and they certainly prefer less expensive properties. If you can find a home that's offered for a great price, especially if the bank in question owns it, they will jump at the opportunity to have someone pick up the tab. It's a better option for them than auctions.

One item of documentation for home mortgage application that is often overlooked is a gift letter. If your relatives have chipped in to help you make your down payment, you may need to document your source of income. This really depends on the type of home mortgage you get. Some require this, and others do not. Play it safe by getting a gift letter from anyone who gives you money to help you buy your home. Have this on file with your other documentation.

Before you apply for a mortgage, consider how much you want to spend. If https://business.chase.com/resources/start/business-checking approves you for a larger amount than what is affordable for you, then this offers you some wiggle room. Nevertheless, you should not overextend yourself. Doing this might mean serious financial troubles later in life.

Be sure that you know exactly how long your home mortgage contract will require you to wait before it allows you to refinance. Some contracts will let you within on year, while others may not allow it before five years pass. What you can tolerate depends on many factors, so be sure to keep this tip in mind.

Do not forget to consider the local property tax rates before you enter into a home mortgage contract. Just because click the up coming website can afford the mortgage payment does not mean that you will be able to afford the taxes on the home. In some areas the taxes on a modest home can feel like a second mortgage, so be sure to look into this.

Understanding the principles of a solid mortgage helps you get the best mortgage for your particular financial situation. Getting a home loan is a major commitment, and you never want to get yourself into an uncomfortable bind. Instead, you want a comfortable mortgage with a company that is going to take care of its homeowners.